From the earliest campaigns against management in the 1920s to the massive raids of Carl Icahn today, shareholder activism has been long considered an American invention. However, shareholder activism is spreading across the globe, and this report from Lazard shows that 2018 was a record year for activist campaigns in a number of ways:

| Global shareholder activism | 2017 | 2018 | Increase |

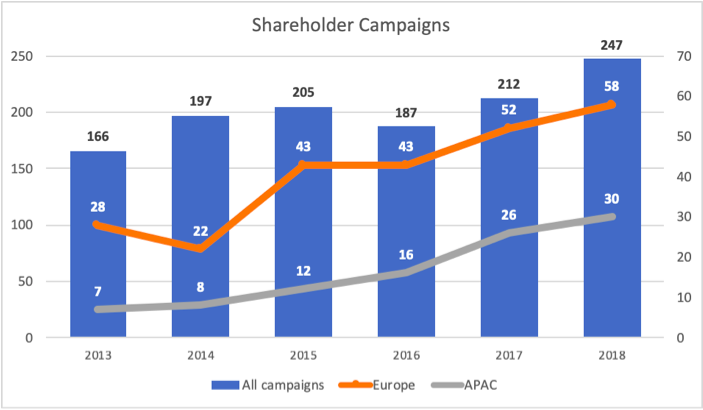

| Number of campaigns: | 212 | 247 | 16% |

| Number of investors:

Number of first-time activists: |

109

23 |

131

40 |

20%

74% |

| Number of targets: | 188 | 226 | 20% |

| Capital deployed: | $64.2 b | $65.0 b | 1% |

Significantly, Europe and the Asia/Pacific region are seeing increases in the number of campaigns waged in those regions. From 2017 to 2018, the number of campaigns in Europe from 52 to 58, while in APAC, the numbers are 26 to 30, respectively. For both regions, these numbers of campaigns are a record high. Moreover, these numbers represent a dramatic increase from five years ago, when there were only 28 campaigns in Europe and only 7 in APAC.

Shareholder Activism: Europe & APAC

Shareholder Activism: Europe & APAC

Why has there been such a major increase in campaigns in Europe and APAC? At least as far as Europe is concerned, European CEO points to a number of reasons. First, hedge funds are increasingly acting as shareholder activists, and many U.S. funds are looking outside of the country for fresh, viable targets. Secondly, European investors—after years of viewing U.S-style shareholder activism as a poor fit for the local culture—have begun to see wisdom in the approach, particularly in the United Kingdom: recent high-profile wins by activists have demonstrated that the activist strategy can work. Internationally, as an Activist Insight survey report notes, it appears that stakeholders are becoming more willing to accept activism than in past years. (Interestingly, the Activist Insight survey also found that shareholder activists are increasingly undertaking campaigns based on social issues in addition to campaigns about corporate performance and governance.)

That said, European investors still go for a more “quiet” form of activism. “Quiet activism can include activists who prefer to influence board decisions by abstaining or withholding votes for proxy issues, or activists who decide to conduct their campaigns with the management in private” rather than launching the full-on, highly-publicized battles that characterize hostile takeovers and buyouts. As shareholder activism goes international, the forms of the campaigns are also undergoing transformation.