Two recent studies on CEO compensation and company performance by corporate-governance firm MSCI and The Wall Street Journal find that there is little correlation between CEO compensation and company performance. But both point to different reasons why.

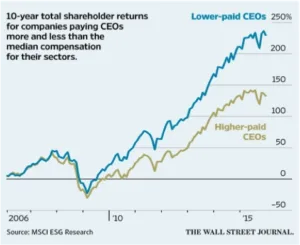

Last month, MSCI published a study comparing the equity incentive pay of 800 CEOs at 429 large-cap U.S. companies to shareholder returns over the past decade. The corporate governance firm found that some of the best paid CEOs ran the worst-performing companies, while many lower paid CEOs managed companies with consistently higher shareholder returns. In fact, lower paid CEOs’ companies outperformed higher paid CEOs’ businesses by up to 39%.

Last month, MSCI published a study comparing the equity incentive pay of 800 CEOs at 429 large-cap U.S. companies to shareholder returns over the past decade. The corporate governance firm found that some of the best paid CEOs ran the worst-performing companies, while many lower paid CEOs managed companies with consistently higher shareholder returns. In fact, lower paid CEOs’ companies outperformed higher paid CEOs’ businesses by up to 39%.

Though equity incentives constitute 70% of CEO compensation in the U.S., MSCI “found little evidence to show a link between the large proportion of pay that such awards represent and long-term company stock performance.”

An article in the Wall Street Journal found a similar disconnect between CEO compensation and company performance. It concluded that CEOs leading the best performing S&P 500 companies last year received the lowest median pay. None of the ten highest-paid CEOs ran any of the ten best-performing companies.

What is causing this disconnect between pay and performance?

MSCI blames U.S. Securities and Exchange Commission (SEC) disclosure rules mandating annual reporting. Annual reporting encourages rewarding CEOs for short-term results instead of longer-term performance. While year-end data is a good indicator of recent performance, this is not necessarily indicative of performance over the long-term.

Unlike MSCI, The Wall Street Journal attributes this incongruity to tying CEO pay to long-term performance benchmarks that overlook periods of poor performance. Many of those protesting excessive CEO compensation do so during periods of economic hardship and poor company performance.

Does it sound as if these studies have come up with opposite conclusions? For one, the period of comparative review should be longer; for the other one, shorter. But maybe it’s neither. Perhaps the review of performance and pay over what are largely arbitrary time periods doesn’t fully align the cause and effect of one person’s leadership. MSCI suggests that to better align CEO pay with longer-term investor interests, the SEC should require disclosure of cumulative incentive pay and performance over a CEO’s tenure. If the frame of a study corresponded with the entrance and exit of individual leaders, this might ensure a closer alignment between leadership and outcome.