This report is published courtesy of the Private Capital Research Institute (PCRI), a non-profit organization that seeks to further the understanding of private capital and its impact through independent academic studies.

The massive inflows of capital into entrepreneurial firms, whether through venture funds or alternative vehicles, has challenged general and limited partners to rethink the traditional venture capital model, their value creation strategies, and their relationship with each other. On July 15, 2018, the Private Capital Research Institute, a non-profit focused on collecting data on private capital and encouraging its use by academics, held a workshop to explore these issues with the Institute for Business Innovation at the Haas School of Business at the University of California-Berkeley on the Berkeley campus. The workshop included discussions with limited and general partners, which are summarized here.

A third part of the discussions featured academics to share their perspectives on the growth of new models in entrepreneurial finance. Ramana Nanda from the Harvard Business School, Rick Townsend from the University of California-San Diego’s Rady School of Management, and Toby Stuart from that University of California-Berkeley’s Hass School of Business presented their research that shows the broad disruptive impact that big data is having across the venture landscape, including investment decision-making.

To begin, Ramana Nanda presented research (work-in-progress with co-authors Christian Catalini from MIT and Chris Foster at Harvard Business School) on the use of machine learning to evaluate applications by early-stage startups to accelerator programs. As the cost of starting ventures has fallen and the number of startups have sky-rocketed in recent years, early stage investors in general and accelerators in particular face an increasing challenge to screen these applications. The vast majority of applications are of low quality, but a few ‘unicorns’ such as Airbnb and Dropbox nevertheless first developed traction by joining accelerators. Nanda and his colleagues sought to assess whether artificial intelligence could be used as a scalable way to effectively to screen the high volume of applications while preserving or even increasing the chances of identifying such ‘needles in a haystack’.

The researchers started with a set of 14,000 applications received by one of the largest accelerator programs in the US between 2013 and 2016. They first collected the amount of money raised by the applicants to the accelerator by December 2017 (as an intermediate measure of success), regardless of whether the applications were accepted to the accelerator program. They then used machine learning techniques, including natural language processing, to study the extent to which success could be predicted from characteristics of the applications, and whether machines could do so more effectively than the human judges. To do so, they trained two sets of models: the first model was trained to mimic the score given to applications by the accelerator’s judges, as a way to replicate the considerations used by the humans when screening applications. A second model was trained to pick the most successful startups as measured by the amount of money raised, regardless of whether judges scored the application highly.

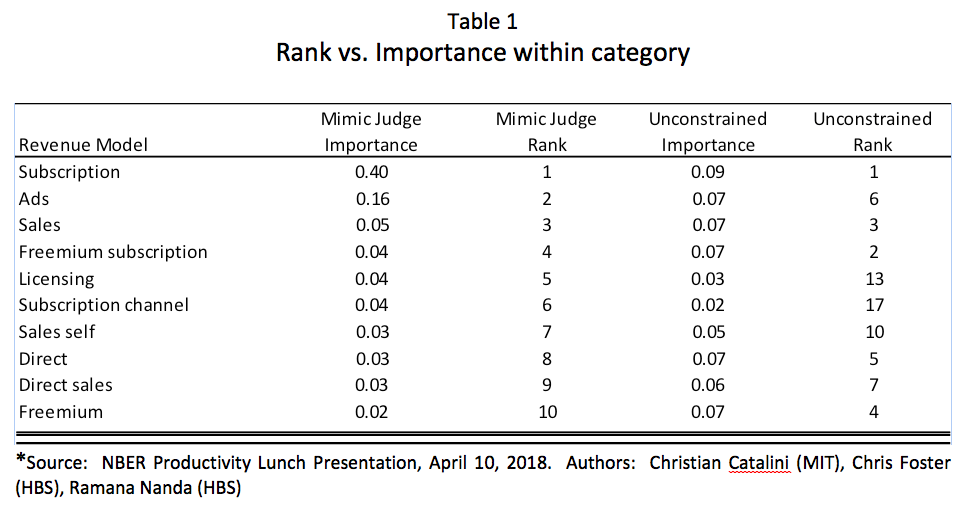

The researchers had three main findings. First, models trained to mimic judges were able to replicate the heuristics of these investors extremely well. Second, models trained to maximize success did significantly better in picking successful ventures than the actual judges (and the models trained to mimic the actual judges). When comparing the emphasis placed on attributes of the applications by the two different models, the researchers found that the model trained to mimic humans tended to emphasize a few variables extremely highly, and entirely miss others. As an example, Table 1 below shows the Rank versus Importance of the various characteristics of the different startups when considering the startup’s revenue model. The model that best mimics the judges, on average, assigned nearly half the total weight to whether the start-up employed a subscription-based business model, showing the human judges strongly prefer ventures with recurring revenue. The ‘unconstrained model’ that maximizes the amount raised also put a high weight on firms with a subscription model, but the weights were more evenly distributed across characteristics. This difference implied that while recurring revenue was important, several other factors were also relevant for success – many that the models mimicking humans did not end up emphasizing due to the large weight but on applications with a recurring revenue model.

Overall, this research suggests that human judges follow an identifiable pattern that can be replicated by machine learning. More importantly, this research finds that machine intelligence, which does not face the cognitive limitations and biases of humans, may do substantially better than human judges in finding successful startups in terms of money raised when processing the large volumes of applications received by early-stage startup financiers.

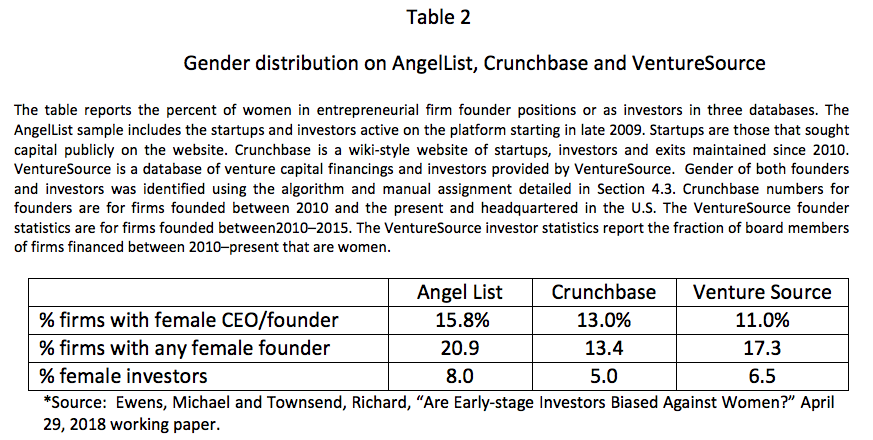

In the second presentation, Rick Townsend described his research[1](with Michael Ewens from Caltech) that explores whether early-stage male investors were biased against female entrepreneurs. The data show that there is a significant gender gap in both VC funds and in VC-backed entrepreneurs: for instance, studies of startup activity in the U.S. find that only 10-15% of funded startups are founded by women. Table 2 below provides a Gender Distribution on investments from three different information sources. Many have speculated that part of the gender gap may, in fact, be due to a lower propensity for investors to fund female entrepreneurs seeking capital.

The researchers use data from AngelList, which provides detailed investor-founder interactions for a large sample of fundraising startups, some of which succeeded in raising capital and some of which failed. Using these unique data, they find that female founders are significantly less successful in garnering interest and raising capital from male investors, as compared to similar male founders. The researchers also find that female entrepreneurs are more likely to be funded by female investors rather than male investors. Lastly, they find that female-led startups are more successful when funded by female investors and, in fact, are more successful than male-led startups supported by male investors. This research demonstrates that there is clearly gender bias in early-stage investments and that in order to boost female entrepreneurship, there needs to be an increase the number of female investors.

Lastly, in the final presentation, Toby Stuart shared his current research (with co-authors Weiyi Ng and Mosche Barach). Toby began by explaining that many leading technology companies in the Silicon Valley have been buying start-up companies. In many of these transactions, the buyer has little interest in acquiring the startup’s projects or assets. Instead, the buyer’s primary motivation is to hire some or all of the startup’s software engineers. In this research, Toby looks at the retention rate of these “acqui-hires” as compared to engineers of similar background and skills who were directlyhired by the firm. Toby first gathers a database of 60 million resumes by scraping LinkedIn profiles and then, using machine learning, he creates two samples of employees who are observably similar: those who were organically hired and those who joined the firm through an acquisition.

Toby finds that the retention rate of acqui-hires in the year of a merger is 50% lower than that of similarly skilled organic hires. He also finds that higher-ranked employees have lower retention rates. Being in Silicon Valley further decreases the average retention rate. Also, he finds that acqui-hires are more likely than organic hires to leave their firms to start their own companies. These results suggest that a strategy by publicly-traded leading technology companies to undertake acquisitions to satisfy the high demand for engineering talent is not a good strategy in the long-term and that the shareholders of these companies lose in the process.

[1] Ewens, Michael and Townsend, Richard, “Are Early-stage Investors Biased Against Women?” April 29, 2018 working paper. Available at SSRN: https://ssrn.com/abstract=2953011